While on the surface, businesses and nonprofits may seem like polar opposites, they actually have a lot in common when it comes to finances. Although businesses operate to make a profit and nonprofits work to make a difference, they both generate revenue and accrue expenses that they must keep track of to keep their organizations operating smoothly.

As a nonprofit professional, managing your organization’s finances is a mundane but necessary part of making the magic of your mission possible. This behind-the-scenes work allows you to develop new programming, pay your staff, and fulfill your nonprofit’s purpose.

Compiling financial statements is one of the main components of proper nonprofit financial management. In this guide, we’ll explore why these documents are so important and the four main types your organization must produce.

Importance of Nonprofit Financial Statements

Nonprofit financial statements summarize your organization’s financial activities and health for both internal stakeholders—like staff, leadership, and board members—and external stakeholders—like donors, sponsors, grantors, and the general public.

When you compile these statements correctly, your organization will receive the following benefits:

- Better decision-making. Compiling nonprofit financial statements allows you to centralize crucial financial information. That way, you can base your budgeting and resource allocation decisions on your pressing needs and current financial trends.

- Enhanced strategic planning. The strategic planning process involves creating a roadmap that aligns your goals with your mission and values. To create this guiding document, you must understand your nonprofit’s current state, including its financial standing. Using the data from your financial statements, you can set realistic, well-informed goals for your strategic plan.

- Improved risk management. Financial statements can illuminate potential risks. Once you’re aware of these issues, you can take action to mitigate them so they don’t negatively impact your nonprofit.

Additionally, nonprofit financial statements allow you to build stronger relationships with external stakeholders. As Double the Donation’s donor stewardship guide explains, “No matter the size of their donation, donors want to know that your organization is using their funds responsibly.” Sharing these documents increases transparency with donors and other stakeholders and keeps your organization accountable for responsible resource allocation.

4 Key Nonprofit Financial Statements

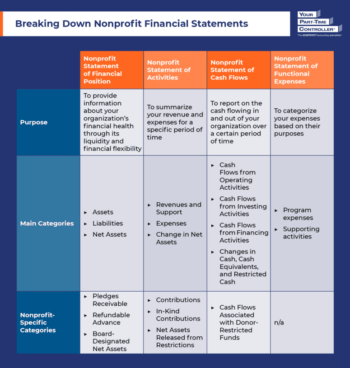

Now that you understand why nonprofit financial statements matter, we’ll explore the four main types of statements: Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses.

Statement of Financial Position

The nonprofit Statement of Financial Position is the equivalent of a for-profit business’s balance sheet. It summarizes your organization’s financial health as of a specific date through its assets and liabilities.

Therefore, the main categories of this statement are:

- Assets. Assets are resources that your nonprofit owns or controls. Your current assets may include cash and cash equivalents, accounts receivable, prepaid expenses, and inventory. Noncurrent assets may include land, buildings, and equipment.

- Liabilities. Liabilities are financial debts or obligations that your organization owes. While current liabilities may include accounts payable, accrued expenses, and deferred revenue, noncurrent liabilities may include mortgages or long-term lease obligations.

- Net Assets. To calculate your net assets, subtract your liabilities from your assets. This number represents the financial resources available to your organization. Positive net assets indicate your nonprofit is in a healthy financial position. On the other hand, negative net assets reveal a need to generate more revenue or cut costs.

While all these categories are included in a for-profit balance sheet, the nonprofit version has three additional categories: Pledges Receivable, Refundable Advance, and Board-Designated Net Assets.

Statement of Activities

The nonprofit Statement of Activities, also known as an income statement, reports your revenues and expenses for a specific period, whether monthly, quarterly, or annually. It serves as a reference for how you’re managing your resources.

This statement includes the following categories:

- Revenues and Support. Revenues and support are funds you generate or resources your nonprofit receives. Revenues may come from selling goods or providing services, whereas support may be in the form of contributions.

- Expenses. Expenses are costs your organization incurs for program, management and general, and fundraising activities.

- Change in Net Assets. Calculate your change in net assets by finding the difference between your revenues and expenses. This metric tells you how your financial resources have changed over the designated time period.

When compiling this statement, separate income with and without donor restrictions into different columns. This way, you can calculate your change in net assets both with and without donor restrictions.

Statement of Cash Flows

The nonprofit Statement of Cash Flows shows how cash flows in and out of your nonprofit over a specific time period from operating, investing, and financing activities.

As a result, the three main categories of this document are:

- Cash Flows from Operating Activities. Cash inflows from operating activities include funds your nonprofit generates from donations, program fees, grants, and membership dues. Cash outflows in this category may include staff salaries and wages, utilities, supplies, and rent.

- Cash Flows from Investing Activities. Proceeds from investment sales or maturities count as cash inflows in this category. Investing activity cash outflows would be purchases of investments, property, or equipment.

- Cash Flows from Financing Activities. Cash inflows from financing activities include lines of credit and loan proceeds, while outflows include debt payments.

Additionally, include a section for Changes in Cash, Cash Equivalents, and Restricted Cash at the bottom of your Statement of Cash Flows. By noting your cash, cash equivalents, and restricted cash at the beginning and end of the period, you can analyze how your cash flows have changed over time.

Statement of Functional Expenses

Lastly, you must report on the nature and function of your expenses. There are multiple ways to document this information. As YPTC’s nonprofit financial statements guide explains, nonprofits “can choose to do this on the face of their Statement of Activities, as a schedule in the notes attached to the full set of documents, or in a separate financial statement—the Statement of Functional Expenses.”

Most nonprofits choose to compile the Statement of Functional Expenses because it organizes this information for when they need to fill out Form 990.

These are the main categories of the Statement of Functional Expenses:

- Program expenses. If a cost is directly related to your services, it falls under program expenses. For example, a disaster relief organization purchasing supplies to rebuild homes would incur a program expense.

- Supporting activities. All other expenses fall under supporting activities, which encompass three main categories:

- Management and general expenses, which relate to your overarching operations and management.

- Fundraising expenses, including costs associated with soliciting donations and securing grants.

- Membership development expenses, which include costs involved in new member solicitation, membership dues collection, and forming relationships with members.

List each expense by its natural classification. Your total expenses should match the total expenses on your Statement of Activities.

While you should now have a better understanding of the four main nonprofit financial statements, you may need some extra help in compiling these statements correctly. Consider working with a nonprofit accounting firm that can take this task off your plate and lend its expertise in nonprofit financial management to your organization.